![]()

Thoughts On The U.S. Shale Gas Revolution

Submitted by RDM Capital on June 12th, 2013Due to new techniques for extracting natural gas from unconventional shale and tight gas deposits, such as “fracking,” the United States is in the midst of a natural gas revolution that has transformed the energy industry in North America. Development of abundant and cheap natural gas has profound implications for manufacturers, consumers and public utilities, and has the potential to drastically impact both the domestic and global economy. At RDM Capital, we are closely monitoring the developments in the natural gas industry as they impact our clients’ interests. Below are a few brief notes about the shale gas revolution. We will also summarize the impact of the shale gas revolution in our upcoming second quarter market commentary.

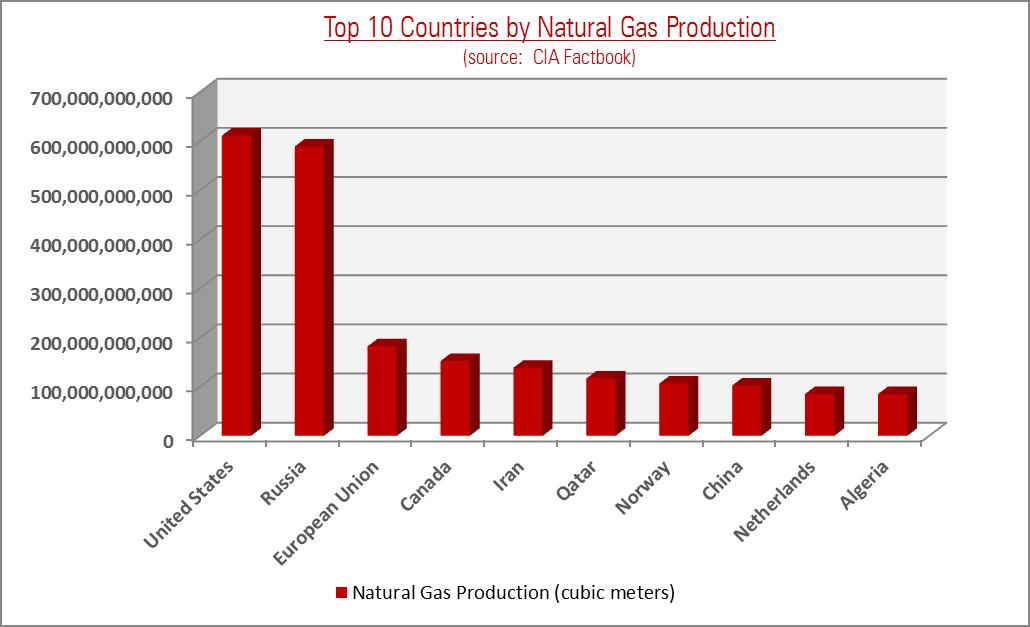

- The United States is now the world’s top natural gas producer, with over 3 times more production than the European Union (see chart, right).

- Unconventional natural gas resources account for approximately half of all natural gas production in the United States.

- The United States could become a net exporter of energy by 2020, according to the International Energy Agency. At the same time, domestic businesses and consumers have switched to natural gas from oil as their primary energy source in areas such as chemical manufacturing, public transportation, freight hauling and utilities. Going forward, the U.S. will become less dependent on foreign oil, which is especially important when one considers the ongoing political uncertainty in the Middle East.

- The government is getting on board. It appears that the Obama administration will allow for construction of export terminals to export natural gas from U.S. to other countries where natural gas is far less plentiful and far more expensive. This support by the Obama administration – an administration that has typically proceeded with extreme caution in traditional energy infrastructure development – reflects recent government studies that conclude that the benefits from exporting liquefied natural gas to foreign countries outweigh the costs associated with higher natural gas prices domestically resulting from the freer trade of the resources.

- Relatively low natural gas prices in the near term will support domestic manufacturers in industries that rely on natural gas as an import cost (i.e. chemicals manufacturing) as they compete with foreign companies that pay relatively higher price for the same input. Over the long term, liquefied natural gas exports from the U.S. to foreign countries will dissipate this comparative advantage.

- Productive plays in the U.S. include the Marcellus shale in New York, Pennsylvania, West Virginia; the Bakken shale in North Dakota and Montana; and the Barnett shale in Texas. Development of these plays supports thousands of jobs in the communities where production is booming. Many of these communities are located in former industrial manufacturing regions that were hit hard by the outsourcing of manufacturing jobs to foreign countries with comparatively cheap labor.

Despite the positive advances discussed above and our optimistic outlook for the industry going forward, the natural gas landscape is constantly evolving. Producers and the government continue to weigh the benefit of increased natural gas production from shale gas with the potential environmental costs of fracking. Simply put, fracking involves forcibly pumping a mix of water and chemicals into shale formations to release gas that is impossible to reach through traditional drilling techniques. Some argue that the fracking process poses serious threats to the environment (e.g. contamination of the water supply) while the environmental studies to date have come to somewhat conflicting conclusions. This topic promises to be a subject of much public interest and debate for years to come.